An Offer in Compromise is an agreement between a taxpayer and the Internal Revenue Service that settles a taxpayer’s tax liabilities for less than the full amount owed. For many taxpayers seeking relief from an overwhelming past tax bill, the most common solution they will hear about is an Offer in Compromise. Some tax relief companies, especially those advertising on the radio and TV, will push an Offer in Compromise as if it were this easy, guaranteed solution.

So if you’ve gotten just this far, you may be surprised to learn that not every Offer in Compromise application is accepted!

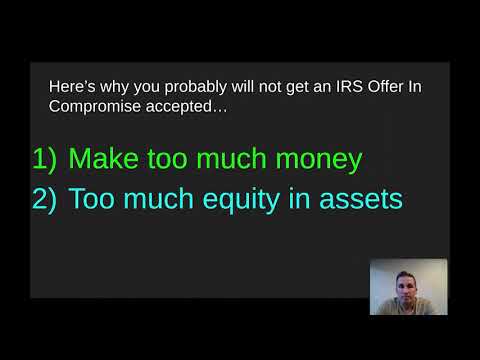

The two biggest reasons the IRS turns down an Offer In Compromise:

- Making too much money

- Having too much equity in assets

Making too much money

In this scenario, the IRS determines you can pay your tax debt off based on how much “available income” you have at the end of the month.

It’s not all based on your actual expenses. The IRS has “collection financial standards” that apply and some people spend more than those amounts.

Example: $100K income, single but nothing left over, and debt is $40K

Having too much equity in assets

The equity in your assets, even if valued at 80%, could pay off your tax debt if the assets were sold. There are some ways to get around this, but as a general rule, it’s how the IRS calculates Offers.

People with assets that are substantial but are broke month to month are good candidates for Currently Not Collectible status, which is different from an Offer in Compromise.

Example: Debt of $100K, 401K valued at $200K

Not sure what to do with your Offer In Compromise? Get a free consultation!

Call us at (888) 515-4829 or go to trp.tax/start

If we cannot help you, we’ll tell you and point you in the right direction.

Going it alone? Check out our free tax help guide by searching “trp tax help guide” on Google.

Need a question answered? Comment on our YouTube videos and a tax attorney will answer.

For immediate help call (888) 515-4829 and we’ll assist you. You can also fill out the form below.