IRS Form 433-B (OIC) is the financial information statement for an IRS Business Offer In Compromise. This 433-B (OIC) guide was written by a tax attorney who is an expert in Offer In Compromise. This post is based on the 2023 form and is part of our free comprehensive tax help guide.

Business Offer In Compromise Financial Statement: IRS Form 433-B (OIC): The Complete Guide

Form 433-B (OIC) is used to determine the ability to pay a business on its IRS tax debts. The IRS is looking to determine if the business is solvent or if it is insolvent to determine the amount it would accept for a settlement. The IRS considers the solvency of the business owner also. Below you can see a video on filling the form out and below the video is the written guide.

Not For All Businesses

Only complete Form 433-B (OIC) for businesses that are a Corporation, LLC classified as a Corporation, Partnership, or Other LLC. Sole proprietorships and LLCs taxed as a sole proprietorship before 2009 should use IRS Form 433-A (OIC) guides Form 433-A (OIC).

Software Considerations and Recommendations

Fill out the form using Adobe Acrobat Reader or Adobe Acrobat Pro. You can download Adobe Acrobat Reader for free here. Do not fill out Form 433-B (OIC) in a browser or another application, it often does not come out properly or has saving issues. Make sure you can save the form before proceeding. Make sure you are connected to a working print and print a test page if you cannot save the forms. You do not want to spend all your time filling it out only for it not to print or save correctly.

Fill It Out the Best You Can

Form 433-B (OIC) should be completed as accurately as possible. When you come across areas you are not totally sure about, use your best estimate. Explain in the cover letter that you used your best estimate for the situation if you are not sure about the item’s accuracy.

Can’t Find Some items

Some people get hung up over one item and never send in the settlement. Get a tax attorney to do it for you or just send it in with your best explanation. If you cannot afford a tax attorney at all just get it in. The IRS will ask for additional information later. If your case is in collections and you need to get it in ASAP, often it is best to just mail it in. Then later add whatever information was missing.

Completing 433-B (OIC) Section by Section

Here we go through the entire form section by section with pictures and written explanations. Below you can watch the video below and it goes step by step through the entire form. You can see the written guide below the video on which the video is based.

Post your questions below in the comment section and they will get answered!

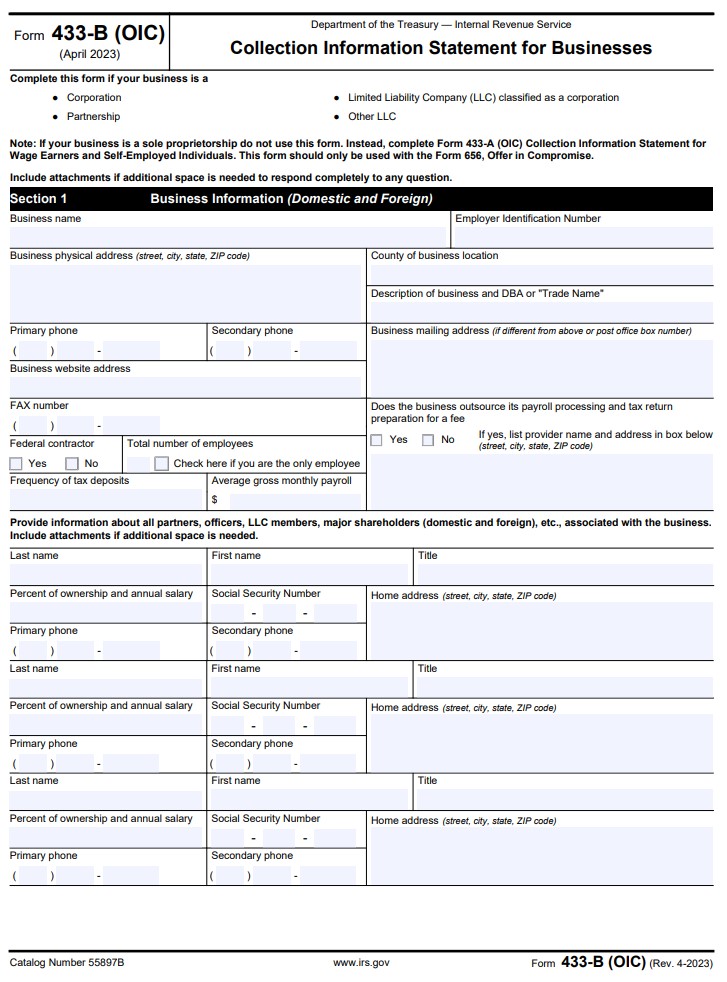

Section 1: Business Information

This section is very basic, everything is self-explanatory for the most part, but I will go over the not-so-obvious sections and add special recommendations.

Frequency of Tax Deposits

This refers to deposits for payroll taxes. Businesses should be using an automated payroll service. Our favorite is Gusto since it is simple and completely online. There is no reason to have an accountant still manually doing payroll. We have had a client’s settlement default because his CPA paper filed payroll returns and one was late. This resulted in having to resubmit the settlement.

Percent of Ownership and Annual Salary

The IRS is trying to see what the owners are getting paid. Say the business has a $1,000,000 tax debt and is claiming to be broke, but the owner collects a $500,000 salary and is single. They usually want to see you adjust things down. It’s their view that if the business is suffering a bit financially and cannot keep up on its taxes, then the owners should not be making a ton of money either.

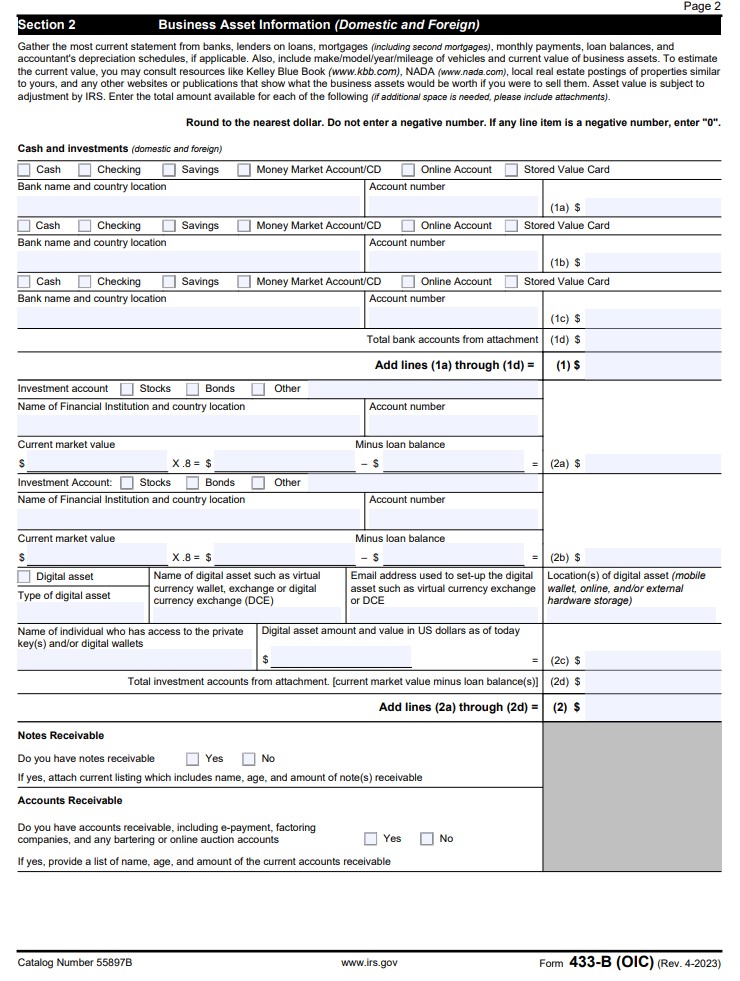

Section 2: Business Asset Information

Here the IRS is looking to see what the business has for assets. Cash, investments, machinery, whatever they deem has some type of value. The key here is quick sale value. Used tools are not worth that much. A vehicle that has mechanical problems or cosmetic issues is worth substantially less than one in good condition.

Cash and Investments

This section goes over basic bank account information to see what cash is in your business bank accounts. Most companies are not going to own stocks or bonds, but fill out this section if any are held by the company.

Notes Receivable / Accounts Receivable

These are simple yes/no questions. The answer for many businesses will be no. Answer yes to notes receivable and you should also attach a list of those notes receivable to your Offer In Compromise. A list is not required for accounts receivable if your business has some when submitting a business Offer In Compromise, but the assigned IRS agent might ask for it later.

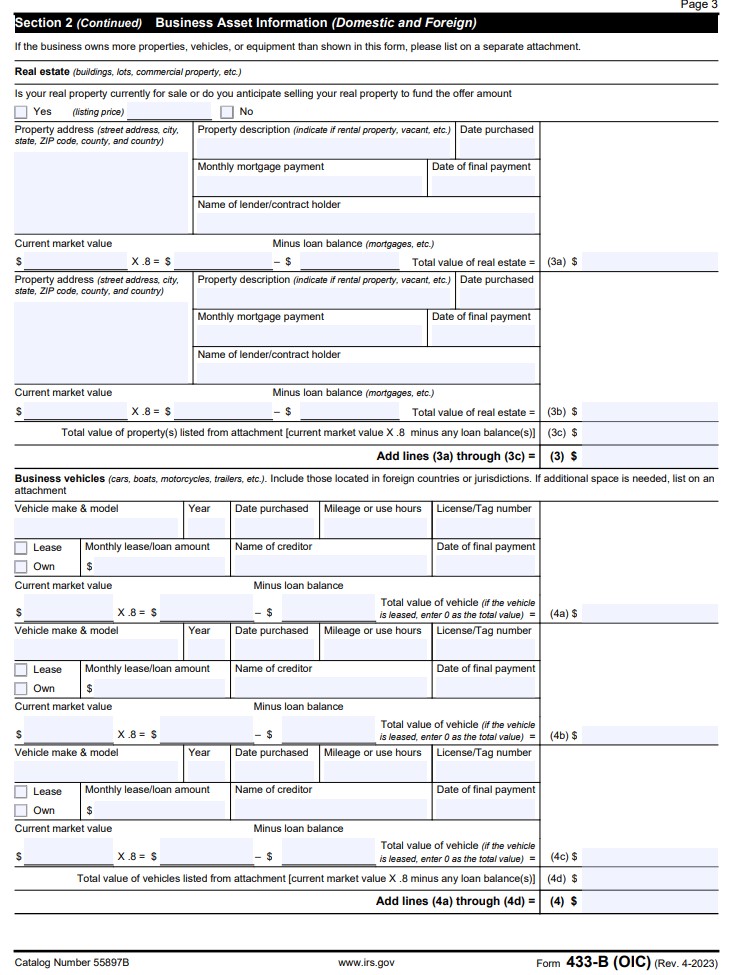

Real Estate – Most Skip This Section

Most businesses do not hold any real estate and should write “N/A” in this section. An Offer In Compromise is extremely unlikely to be accepted if the business owns real estate and the equity is more than the tax amount due. Make sure that if you do include real estate here, you value it with any flaws and defects the property has. Most properties are not perfect, and you want to give an accurate valuation.

Business Vehicles

The same logic applies here. You want to discount the vehicles for any problems and cosmetic issues that they have. Do a comparison on KBB and Edmunds. Pick the lowest one. For purposes of settlement, it is better to lease.

Pro tip: If the IRS later argues that payment is ending so it should not be considered an expense here are the best counter-arguments to get the expense included: If leased: By the time the lease is up and a new vehicle is needed. If purchased: The vehicle will be so old and run down by then, a new vehicle will be needed by the time this payment is up.

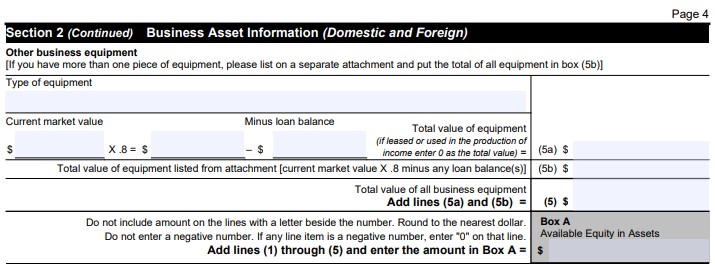

Other Business Equipment

These are tools for your trade and related items. Operating equipment should be included here. Again to be clear, quick sale value should be used. Tools that are used are worth much less than new tools in the packaging. The same thing goes for any type of machinery.

Box A – Available Equity in Assets

Box A is everything totaled up related to assets for the business after allowing certain deductions by the IRS. The amount in Box A, if calculated correctly, is what the IRS believes is the reasonable collection value of your business assets. If Box A is more than your tax debt you probably are not getting an Offer in Compromise accepted.

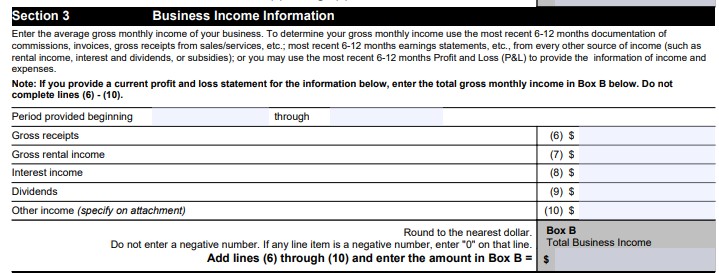

Section 3: Business Income Information

Form 433-B(OIC) gives the IRS how much gross income your business generates on a monthly basis in Section 3. This section is filled out in two ways. One way is if you have a profit and loss statement. Another way if you do not. Enter figures as if they were monthly amounts. For example, if you have a Profit/Loss Statement covering the last 6 months, then divide the number totals by 6.

With Profit/Loss Statement

Many businesses will have a profit/loss statement or can easily make one. In that case, you skip lines 6-10 and fill in the total gross monthly income in Box B.

Without Profit/Loss Statement

If there is no profit/loss statement, fill out the information based on the last 6-12 months. It’s best to put the range of months that produces the lowest average monthly income. Enter the average monthly gross income per category. Most businesses that are filling this out and do not have a profit/loss statement will just be filling out Box 6 and Box B.

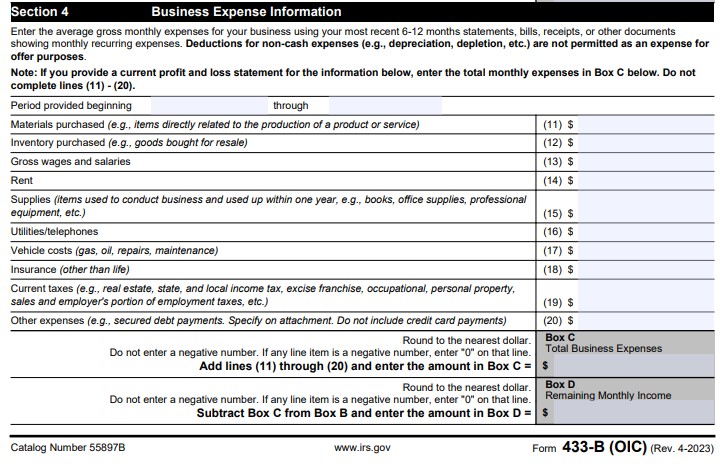

Section 4: Business Expense Information

Section 4 of Form 433-B(OIC) determines the total average monthly expenses for your business. The total will then be deducted from Section 3’s total to find the net monthly profit of your business. Filling out this section also differs depending on whether or not you have a profit/loss statement for your business. Enter figures as if they were monthly amounts just like Section 3.

With Profit/Loss Statement

Go straight to Box C with the total expenses from your profit and loss statement figured to a monthly number. Skip lines 11 through 20.

Without Profit/Loss Statement

Fill in categories 11 through 20 based on your actual expenses over the last 6-12 months. Enter the monthly average for each figure. For other expenses, including an attached list of the expenses.

Box D: Monthly Business Profit

Subtract Box C from Box B and enter it into Box D. This is the monthly profit for your business and is used later in your total offer calculation.

Special Considerations On 433-B(OIC) Sections 3 and 4

Here is where our expertise as tax attorneys comes in and these are the things we consider when evaluating cases for Offer in Compromise that apply to these sections you will not hear about from the IRS or an unlicensed ” tax consultant.”

Gross Rental Income, Interest Income, and Dividends

These are Section 3, Lines 7, 8, and 9. The catch with these categories is most businesses that have any of these categories of income often have more assets than the tax balance due. This makes them ineligible for a financials-based Doubt as to Collectibility Offer in Compromise. Doubt as to Liability Offers in Compromise is extremely difficult.

Financials-based is the way to go if your business qualifies. The exception to this is office owners or lessors that are subleasing out some of their offices. That’s still considered rental income but often is not due to an owned asset.

Gross Wages and Salaries

This is Section 4, Line 13 or should be listed on your profit and loss statement if these are paid out. The IRS agent will be looking to see what the officers are getting paid. They want to see that the company’s officers and owners are not making a lot of money and still trying to get an Offer in Compromise.

Example: Doe Corp owes $100,000 in tax debt. John Doe’s salary is $250,000. He is the sole owner and that is still paid consistently. The IRS probably will not grant an Offer in Compromise to Doe Corp. The agent says John should cut his salary to pay the tax due.

Other Expenses

This is Section 4, Line 20. You need to make sense of this section. Do not add expenses that are not business expenses. If it’s something specific to a certain type of business, it is best to explain it in the attachment in addition to listing it. Present everything upfront and clearly. It makes acceptance more likely than keeping the IRS agent guessing what you sent and asking more questions.

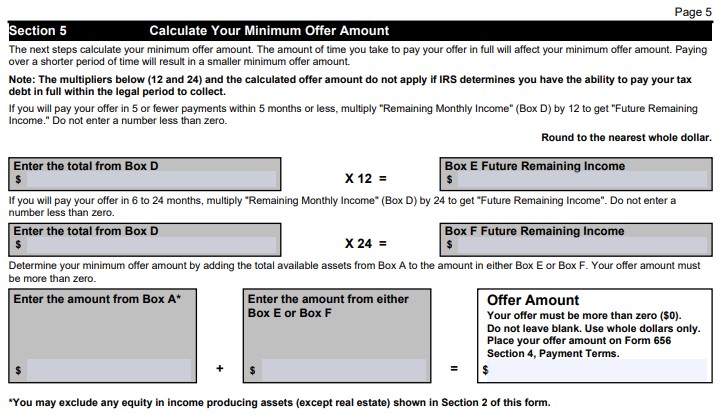

Section 5: Calculate Your Minimum Offer Amount

The totals from the Boxes calculated above are used to calculate the minimum offer amount for your business. The amount is supposed to represent the lowest amount the IRS will accept to settle your business tax debts in full.

Page 5 has Section 5 and the first part of Section 6 on it.

We almost always recommend doing a 5-month payoff Offer in Compromise. The only exception is when your available business income is $0 and there are assets that are being considered in the calculation. You end up paying twice as much to buy the extra time. If you are stuck between these two offers and cannot make payment within 5 months, it is strongly suggested to see who you can borrow from to make it happen, since you save double in the end.

The Actual Offer Calculation and Offer Amount

Paying off within 5 months:

Box A + Box E = Offer Amount

Paying off within 24 months:

Box A + Box F = Offer Amount

Box A is the total available business assets. The total is then added to Box E or F, depending on how long it takes you to pay it off.

The most common reason a 5-month payoff Offer is preferred

A 5-month payoff is the recommended reason in probably 95% of the cases we work on that qualify for an Offer In Compromise, in both business and personal cases. Here are the reasons we prefer a 5-month payoff to a 24-month payoff:

- The overall amount paid to IRS is lower. Half if there is available income.

- IRS liens can be withdrawn faster. Releases also happen faster, but a withdrawal is better.

- Fewer chances for payment to get skipped and mess something up.

- Payments are required while the settlement is pending. This is huge. Debts can be expiring soon. Money paid on debts that were in Offer In Compromise, then rejected, then expired in Currently Not Collectible status, is wasted money.

An example of when a 24-month payoff Offer would make financial sense

John Doe’s business is refurbishing classic cars. The business owns one classic car that still needs work, a 1967 Mustang. It is worth $15,000 and has no loans on it. The available business income is $0 per month. John knows if he fixes up the Mustang he can probably sell it later for much more. John has no way of paying $12,000 within 5 months unless he sells the Mustang. $12,000 is 80% of the value of the vehicle, which the IRS determines is John’s reasonable collection potential. Instead, John goes for a 24-month Offer, and pays the $15,000 over 24 months, in monthly installments of $500.

Pro tip: You can always start with a lower 5-month offer, then later change it to a 24-month Offer when dealing with the IRS agent. This stops you from having to make payments while the Offer is pending, even if you think the 24-month payoff Offer is what you will end up with. Give a reason the assets should not be considered and sometimes it works, sometimes it doesn’t. You then end up with a much lower Offer than the 24-month payoff.

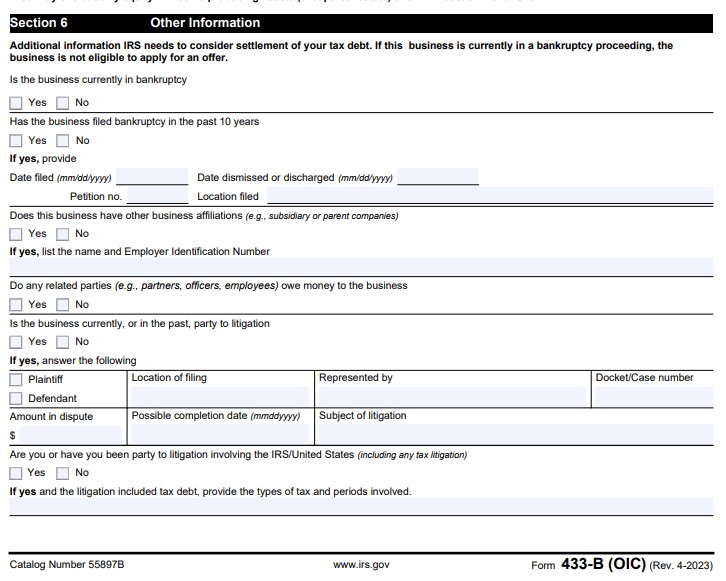

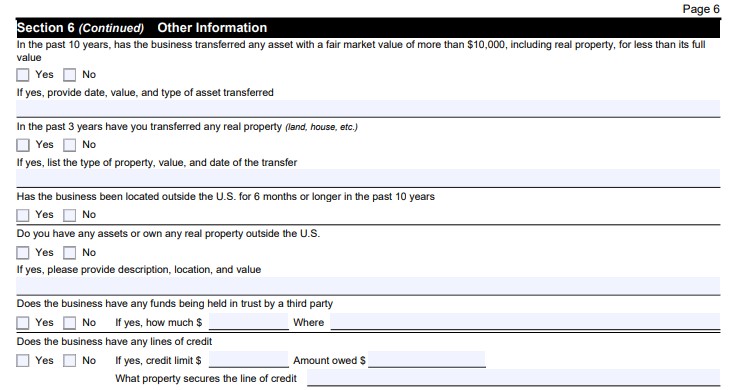

Section 6: Other Information

This section of Form 433-B (OIC) asks general questions about the business and its legal history. The questions are self-explanatory. Litigation that benefits the business or assets sold/transferred for less than full value is what the IRS is looking for.

Examples of situations where the IRS may use this information against you

Past Litigation

The business won a lawsuit and received $1,000,000 one year ago. The business tax debt is $500,000 and became owed two years ago. The IRS will weigh this against the business and an Offer in Compromise is less likely.

Pending Litigation

The business is a Plaintiff in litigation for a failed contract and you have good odds of winning the case. The business will get $1,000,000 plus attorneys fees. The tax debt is $250,000. The IRS agent may say we should wait and see what happens, rejecting your Offer in Compromise.

Transferred Assets

Doe Industrials Inc. owned the office of the business in 2017. It was sold in early 2018 before the Offer in Compromise was submitted, but after the taxes were owed, the fair market value of the building at the time of sale was $500,000. The office was sold to the business owner’s mother for $250,000. The IRS may value the building at $400,000, which is 80% of the value at the time of sale. This creates a $150,000 gap the IRS will treat as available in the business’ Offer in Compromise calculation.

Money Owed To Business and Other Funds

The total business tax debt is $250,000. One partner owes the business $400,000. The partner is solvent and has a net worth of $2,000,000. The IRS is less likely to accept an Offer In Compromise here.

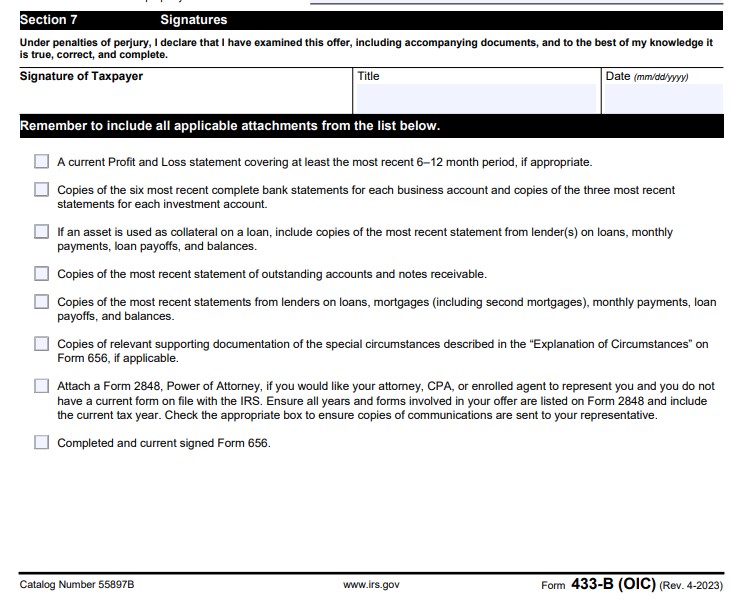

Section 7: Signatures

Here the business owner should sign, put their title, and date the document. Make sure to do a wet signature with a real pen. Sign with blue ink. Failure to include signatures will result in a rejection of IRS Form 433-B (OIC) and your settlement.

Attachment List for Form 433-B (OIC)

This final part of Form 433-B (OIC) lists the documents you need to include with the settlement package. Form 656 should be in there too, as well as checks for the down payment and processing fee. Send copies of the below information. Below is a pasted version of their list, with my notes in bold:

- A current Profit and Loss statement covering at least the most recent 6–12 month period, if appropriate. You can often use last year’s tax return Profit/Loss statement to get around this requirement if it is not too late in the year.

- Six most recent bank statements for each business account and copies of the three most recent statements for each investment and retirement account. Make sure to send the actual statements that show your business address on them. If your bank account balance had a recent drastic change you want to show that is not in the most recent statement, print out the most recent transactions as well, but still include the last six full statements of all accounts.

- If an asset is used as collateral on a loan, include copies of the most recent statement from lender(s) on loans, monthly payments, loan payoffs, and balances.

- The most recent statement of outstanding notes receivable. Notes receivable is money owed to the business.

- Most recent statements from lenders on loans, mortgages (including second mortgages), monthly payments, loan payoffs, and balances

- Relevant supporting documentation of the special circumstances described in the “Explanation of Circumstances” on Form 656, if applicable. Most will not be filling this part out.

- Attach a Form 2848, Power of Attorney, if you would like your attorney, CPA, or enrolled agent to represent you and you do not have a current form on file with the IRS and it is a red flag if this is being sent with your settlement. Many tax relief firms do not call IRS Collections or put a Power of Attorney on file before doing anything on your case. The Power of Attorney should already be on file if someone is doing this for you. If they are not on file, they probably did not check up on collection statute expiration dates, which is very important, and filing an Offer can be the wrong thing to do in some cases even when it looks like an easy approval.

- Completed and signed Form 656. This is the IRS settlement form.

Final Notes and Suggestions: IRS Form 433-B (OIC)

The IRS wants to see that the business is barely making it by way of Form 433-B (OIC). The officers and owners should not be making a ton of money. Just like they want to see the same thing for an individual Offer in Compromise on Form 433-A (OIC). Many of you reading this guide may also be looking to do an individual Offer and if so see our Personal OIC guide here.

Make Copies and Send Certified Mail With Return Receipt

Make copies of everything you are submitting and save it. My final suggestion is to send all mail correspondence to the IRS by USPS Certified Mail with a Return Receipt. Sometimes, but not often, the IRS loses things you send them. The return receipt is valid proof they got it. Use the proof in case they try to reject your case based on not sending something. However, if they lose the document just send it to them again. Fighting them about them losing it will just cost you more time. Keep copies.

If you do not want to go it alone, schedule a free consultation with one of our expert tax attorneys by submitting a request on our Contact page, or call us at (888) 515-4829 and we’ll be happy to assist.