Here we go through getting tax relief. We will walk you through the process of selecting the right resolution for your tax debt from start to finish. Parts of this guide will go into other sections of our site that will cover relevant forms. Follow this guide and complete the required steps and you will get real tax relief.

This guide does not constitute legal advice and proceeds at your own risk. Consult with a licensed tax attorney if you are unsure about anything. See our video explanation below and keep reading for a more in-depth guide to tax relief.

UPDATE 5/20/2021: IRS payment plans are now easier for large balances and updates are reflected below.

Selecting The Best Tax Relief Option

Tax relief first should be divided into two categories: tax debts that are final and tax debts that are still in dispute. Debts that are final would be those where the amount is not in dispute, meaning there is no audit or pending change of the tax return ongoing. Debts that are not final would be those that are still in audit or under some other type of review. Finalized tax debt tax relief options are what most people are looking for, but we will cover both here in this post.

You can also have someone do it for you. Tax attorneys are recommended over tax relief companies since they won’t close on you. You may also be interested in our posts related to this topic: how to prevent and release IRS garnishment.

Tax Relief for Finalized Debts: Offer In Compromise is the best option

When the debt is not in dispute, there are the following tax relief options:

- Offer In Compromise

- Currently Not Collectible

- Payment Plan

- Pay in Full

Offer In Compromise is the best option for those that qualify, and we will go through the basics of qualification for that first, then proceed to the other tax relief options.

Offer In Compromise works when assets and income are low compared to the debt total

The first thing to look at is assets. If you have more assets than the tax debt, your chances are not that good. There are exceptions and we have had Offers approved when a client had a very low-value home, when a property could not be sold after being listed, and when the property was needed to make income.

Second, income is taken into consideration. Your income must barely cover or not cover your expenses unless you have an extremely large debt. If you are single making $100,000 annually and you owe $50,000, you most likely are not getting an Offer In Compromise approved. If you owe $1,000,000 there is a good chance of acceptance, but it will be a large settlement amount

More dependents increase the chance of Offer acceptance. The IRS uses figures based on how many dependents are living in your household. The more the better when it comes to your odds at getting an Offer In Compromise.

Dissipated assets can ruin your Offer

If you cashed out a 401K or sold something significant in the last 3 years and did not pay taxes on it, the IRS will treat it as a dissipated asset. This means they calculate it into your settlement whether or not you actually have the funds. They think since you had the money in hand, you should have paid then.

Example: Sold off all stocks and cashed in $150,000. IRS debt is $50,000 and it has only been one year. The IRS won’t accept an Offer In Compromise in most cases.

If you feel that you are barely or not covering expenses and you have a lower than average income for your area, there’s a very good chance you will get an Offer In Compromise accepted. See our complete Offer In Compromise guide for more information if you think you qualify. It is updated yearly with the latest forms.

Old tax debts sometimes should be handled differently

If you have old tax debts, see our tax debt expiration guide for more information before proceeding on an Offer. You may choose to go with Currently Not Collectible as explained below.

We can also do it for you, but we don’t recommend waiting to hire someone if you cannot afford it. Just get it in. Many people call us when they finally get a higher-paying job and then they don’t qualify. If your Offer is not perfect the IRS will just ask for additional info. We can review your Offer as well as a lower-cost option.

Currently Not Collectible Status: Tax Relief When You Got Assets or Old Debts

This tax relief option is often recommended by IRS agents who fail to mention Offer In Compromise. It’s effectively a payment plan for $0. The debt is still owed, but at some point, it will expire. Sometimes a case can be put into this status and no payments will be made until it expires, effectively creating a lower payment than an Offer In Compromise.

Currently Not Collectible is the best tax relief option if you have assets, but low income or if you have old tax debts that are going to expire soon. Filing for Currently Not Collectible status and having a tax debt of over $10,000 will result in a Federal tax lien. The lien does not necessarily mean anything will get taken away, it just secures their interest. We’ll go through both scenarios.

Too Many Assets For An Offer In Compromise or Dissipated Assets

If you have more assets than the tax debt you probably are not getting an Offer. The same applies if you have dissipated assets as explained above. However, often you can submit for Currently Not Collectible and get approved without having to sell off anything. After computing your income and expenses, if your available income is determined to be $50 or less per month, you probably will get approved.

We have seen the IRS request people to pay out what is in their bank account or retirement account, but not always. We recommend mailing in the request if you have a 401K. It seems when mailed in they are less likely to ask you to cash it out.

Example: Own a home that is paid off of high value, but per month barely making expenses. Currently Not Collectible is probably the best tax relief option.

Tax Debts Expiring Soon

IRS debts have an expiration date. Things can extend that date as well. If your debt is set to expire soon, submitting an Offer In Compromise will extend the amount of time the IRS has to collect. Currently Not Collectible does not extend the statute except for the brief period where the IRS is processing your request as long as your request is based on the information you submitted.

If your account was placed in Currently Not Collectible because you were out of the country and did not submit financial information, the debt expiration period may get extended. The downside of Currently Not Collectible is that after the debts expire, tax liens will get released but not withdrawn. However, having a released lie

Example: You $100,000 for 2009 and it expires in May of 2020. It currently is May 2019. It might be better to just get Currently Not Collectible and let the debt expire.

See our guide on Currently Not Collectible for information on how to proceed with this tax relief option.

Payment Plans: Tax Relief Made Simple

Doesn’t qualify for an Offer or Currently Not Collectible seem unattainable?

Then a payment plan is an easy option. If you can’t or do not want to pay it in full, you can put your balance into an IRS payment plan. It is tax relief in the fact that it will stop garnishments and bank levies from occurring and also release any existing garnishments. The three categories of IRS payment plans:

- Paid over 72 months for balances under $50,000

- Paid over 84 months for balances between $50,000-$100,00

- Payment plans where you owe over $100,000 and other payment plans that require the submission of a financial statement because you cannot afford the payments on the 84 months or 72-month payment plan

The type of payment plan you get is based on how much you owe and whether or not you can make a minimum payment that the IRS is requesting. If you cannot make the minimum payment that they are requesting, then a financial statement will be required.

Payment plans for balance under $50,000

When you owe less than $50,000 but otherwise don’t qualify for a Currently Not Collectible or an Offer in Compromise, you may just want to request an easy payment plan over 72 months as long as you pay it off over 72 months. The IRS does not require a financial statement. They will go ahead and they do not issue any liens on top of that you can request the penalty abatement at the appropriate time.

Payment plans between $50,000 and $100,000

The balance can be spread out over 84 months. The IRS will not request a financial statement from you. However, the IRS will file a lien at this balance amount. The only way to avoid a lien in this situation is to pay the balance below $50,000 and then put it in the 72-month payment plan as we explained above. You can also request a penalty abatement once you come close to paying off the first year you owe.

Payment plans under $250,000

As a part of the IRS Fresh Start program, the IRS now accepts any payment plan that pays the taxes off before the tax debt expires (also known as the Collection Statute Expiration Date). Tax liens will still be filed under this payment plan scenario as long as the balance is over $50,000.

Payment plans over $250,000

When you over $250,000 unless you can pay it down below $250,000, the IRS is going to require a financial statement. The amount you pay per month will be based on the data on the financial statement. There are some cases where Currently Not Collectible doesn’t end up happening and someone cannot afford the Offer in Compromise number, so they often end up in payment plans that do not pay off the balance in full because the balance expires before the debt is paid in full. In a way, it is almost like a reverse Offer in Compromise.

When you owe more than $250,000, you’re not going to easily get an Offer in Compromise or Currently Not Collectible status unless your financials are simple. Attorneys are strongly recommended to handle these kinds of cases. In this type of payment plan, you can also request a penalty abatement.

Submitting a financial statement

When you don’t qualify for an Offer in compromise or Not Collectible yet you still cannot make the minimum monthly payment that the IRS is requesting for the 72 or 84 month plan, then you need to submit a financial statement. We have found that in most cases like this we can usually find some way to get the client an Offer in Compromise. A lot of times there is an expense that is not considered or there was an expense that the client can add that is valid that would make them qualify for an Offer in Compromise.

If you find yourself in this category, definitely give us a call so we can go over your case and see if we can make an Offer In Compromise happen for you, in a legal way of course. These type of payment plans often do end up being similar to Offer in Compromise because the tax may expire before you finish paying it off.

Resolving IRS debt with a payment plan

See our in-depth guide on IRS payment plans for more information if you are taking this route of tax relief.

Paying the IRS in full: Often best if you can do it

If you have money sitting there, might as well pay it off. You will not get an Offer In Compromise and the payment plan will just add penalties and interest. Some may have something else the money is going to or an investment that will make them more than the IRS penalties and interest rate. In that case, you still might go with a payment plan.

Penalty Abatements: For payment plans and full payers

Those paying in full or in a payment plan will want to request a penalty abatement. It’s easy to get on the first year that you owe on if the prior 3 years do not have a previous penalty on the account. The IRS will grant a “first-time penalty abatement” based on prior compliance. For any other year, you have to show “reasonable cause” according to the IRS.

We inform clients that “reasonable cause” can be hard to prove and don’t count on getting out of penalties for the other years if you are doing a full payment or payment plan.

See our first-time penalty abatement guide for more information.

Tax Relief For Debts That Are not Finalized or Wrong

Some tax debts may not be completely finalize

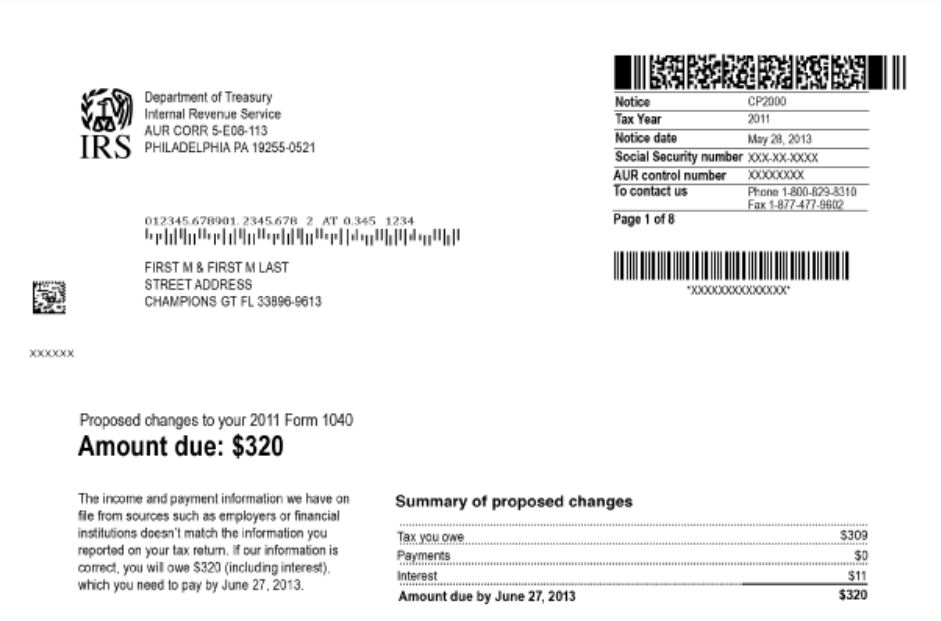

These tax debts might be under audit or you may have received a CP2000 notice requesting information or adding tax debt to your balance. These are not yet finalized because you either have not signed off in approval of the change, or IRS has not entered the change by default due to your lack of correspondence.

You may also be in the middle of an auditor in the mix of responses with the IRS and these debts might not be finalized. The tax relief goal in these cases is to lower the debt as much as possible before it becomes final.

You receive a CP2000 when the information you reported on your tax return does not match records that were sent to the IRS from another source

Audit reconsideration is a request to the IRS to reconsider their previous determination. Sometimes you may not have received the audit paperwork or at the time you did not have the documentation. Although it is not a right to have a reconsideration, the IRS does not want to stick you with the debt you really do not know so if you can prove it with proper documentation it’s very likely they will approve a reconsideration.

What you can do in an audit, CP2000 notice, or reconsideration to get tax relief

For an open audit or CP2000, you need to provide all the information the IRS is requesting. As long as your information is properly documented and you can show proof of expenses, it’s very likely there will be no change to the audit. If everything is not documented properly and it’s hard to put everything together you probably want to call a tax attorney to help you with the audit.

If an audit has already taken place or CP2000 notice was already closed out but you think everything was wrong you may want to do an audit reconsideration. However, you must have good documentation to prove that you really do not owe the debt. If you don’t have proper documentation and a good explanation, it might not be worth your time.

When the audit reconsideration won’t wipe out the debt anyway

If you were audited or had a CP2000 notice that added a significant balance and doing an audit reconsideration would only slightly reduce the balance, you may want to look if you qualify for an Offer in Compromise first. If you’re going to get an Offer in Compromise anyway, it might not be worth the headache to go through an audit reconsideration if it’s really not going to wipe out the balance. The truth is, an Offer in Compromise will wipe out the debt completely and it’s based on your financial information. So if you qualify, it’s easier to go with the Offer first.

Example: You have a tax debt of $100,000. If you win your audit reconsideration you would have a tax of $50,000. You already qualify for an Offer In Compromise for $100. There is no point to submit the audit reconsideration. If you get the Offer in Compromise, it wipes out the entire debt and is based on your financial information, not the balance total.

Concluding our guide on Tax Relief

Tax relief is a complex subject. If you pick the right resolution and follow through with the paperwork, you should see some results. If you do have a complex case, doing it yourself might be a headache. You might be better off just hiring a tax attorney. However, if you’re not in a financial situation to hire help, we recommend you to go proceed with a resolution.

You often will get the best resolution when you’re making the least amount of money. The more money you make the less likely you are to get an Offer in Compromise. The less money you have, the more likely you are to get away with paying the IRS less.

Getting help is easy

At the same time, many tax relief services are more affordable than you may think. Our firm’s fees are very affordable and we only charge you for the time that we spend in your case. You won’t be charged a percentage of how much is owed. We only charge you the time it takes to get you the best result possible. If we can get you a settlement will let you know quickly and if not, we’re not here to waste your time or money.

That being said, if you are struggling financially and think you qualify for an Offer, just get it in ASAP and use our tax help guide to walk you through the process.

Don’t want to do it yourself? Go to our contact page or call us at (888) 515-4829.

For immediate help call (888) 515-4829 and we’ll assist you. You can also fill out the form below.